Will Conforming Loan Limits Change In 2021

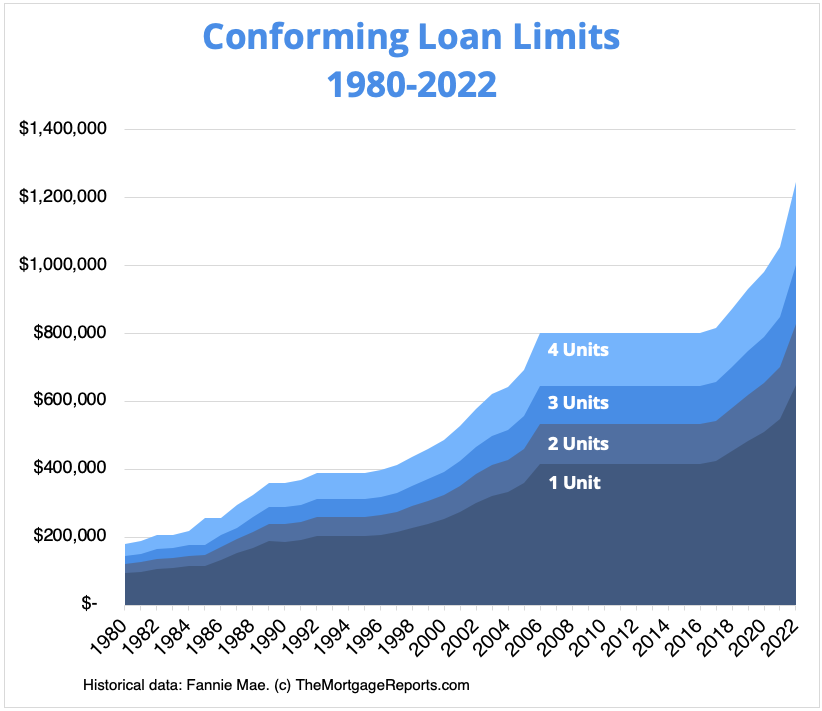

Befitting loan limits ascension past near $100K

Habitation prices rose at a record pace in 2021, putting force per unit area on buyers to get bigger and bigger mortgage loans.

Luckily, loan limits are keeping pace with dwelling house price aggrandizement.

Starting January i, 2022, the new conforming loan limits volition attain up to $647,200 in nigh of the U.S. and $970,800 in loftier–cost areas.

And you don't have to wait until 2022 to take advantage. Many lenders are already offering higher loan limits today.

In this article (Skip to...)

- 2022 Loan limits

- Loan limits map

- How loan limits work

- Well-nigh befitting loans

- Nearly jumbo loans

- FHA loan limits 2022

- Today'southward mortgage rates

Conventional loan limits for 2022

Lending limits for conventional conforming loans got a huge boost this year.

The Federal Housing Finance Agency (FHFA) determined habitation prices are upwardly by more than 18% on average across the nation.

Information technology raised conforming loan limits by the aforementioned percentage – a dollar increase of almost $100,000 for the standard ane–unit home. Multi–unit properties got a similar increase.

| Low-Toll Area | Medium-Cost Area | High-Cost Area | |

| ane Unit | $647,200 | $647,201-$970,799 | $970,800 |

| 2 Units | $828,700 | $828,701-$1,243,049 | $i,243,050 |

| 3 Units | $1,001,650 | $ane,001,651-$one,502,474 | $1,502,475 |

| 4 Units | $one,244,850 | $one,244,851-$1,867,274 | $1,867,275 |

Baseline befitting loan limits

Standard loan limits for 2022, which apply in most of the United States, are as follows:

- ane–unit homes: $647,200

- two–unit of measurement homes: $828,700

- 3–unit homes: $1,001,650

- four–unit homes: $1,244,850

Keep in mind that these are simply the 'baseline' limits. In areas with high–cost existent estate, buyers go significantly higher conventional mortgage limits.

Maximum conforming loan limits

High–residual conforming loan limits vary past county. They can autumn inside the following ranges:

- ane–unit homes: $647,201–$970,799

- ii–unit of measurement homes: $828,701–$1,243,049

- 3–unit homes: $1,001,651–$ane,502,474

- 4–unit homes: $1,244,851–$one,867,274

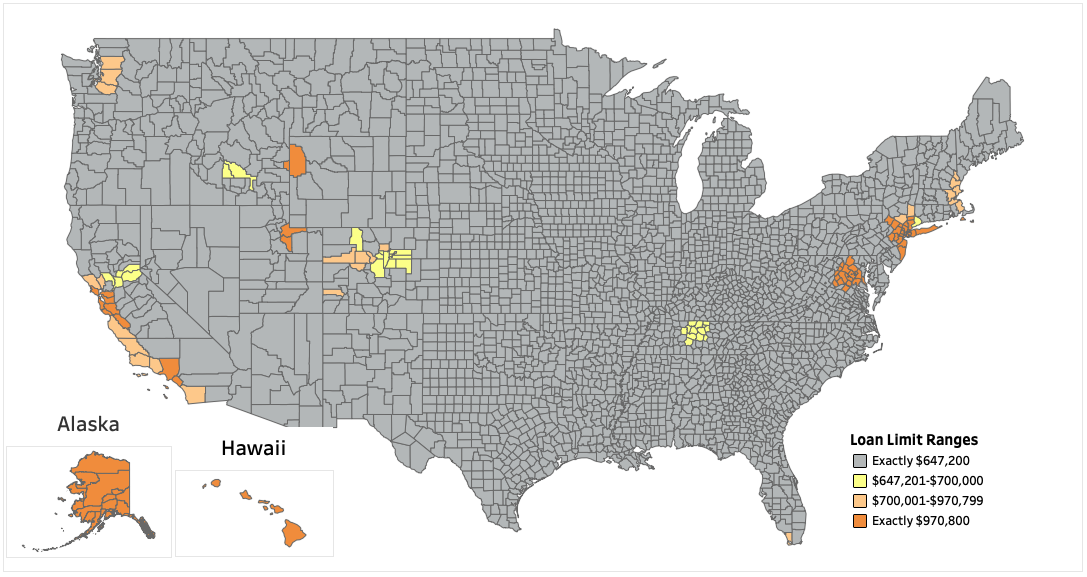

Areas such as Alameda County, California; Arlington, Virginia; and Jackson, Wyoming enjoy the maximum befitting loan limits, while cities like Seattle, Washington and Baltimore, Maryland autumn between the "floor" and the "ceiling."In Alaska, Hawaii, Guam, and the U.South. Virgin Islands – which follow their own loan limit rules – the baseline loan limit for 2022 is $970,799 for a one–unit property.

Conforming loan limits by county for 2022

The post-obit map shows befitting loan limits by county. You lot can see an interactive version of the loan limits map on FHFA's website.

What is a mortgage loan limit?

A loan limit is the maximum corporeality you tin borrow under certain mortgage programs.

In that location is non merely one loan limit, merely many.

Conventional mortgages adhere to one set up of loan limits, and FHA another. VA loans essentially did away with limits in 2020.

In the world of befitting loans, Fannie Mae and Freddie Mac limit "borrowable" amounts to go along their nationwide programs available to those who need them.

For instance, Fannie Mae doesn't desire a $10 million loan going through its arrangement. That's a lot of adventure wrapped up in ane transaction, and the bureau would rather upshot many smaller loans to many home buyers.

Fortunately, loan limits are on the rise in 2022 to reflect ascension dwelling prices across the country.

What is a conforming loan?

A conventional conforming loan is any mortgage that:

- Is not backed by the federal government (meaning it'due south non an FHA, VA, or USDA loan)

- Has a loan amount inside local befitting loan limits

- Meets lending guidelines set by Fannie Mae and Freddie Mac

Mortgages within conforming loan limits are eligible to be backed by Fannie Mae and Freddie Mac, every bit long as the borrower meets basic criteria for credit score, income, down payment, and debt levels.

Conforming loans typically require:

- A credit score of at least 620

- A debt–to–income ratio below 43%

- A downwards payment of at to the lowest degree 3%

- Two–year history of stable employment and income

Exact conforming loan requirements tin vary by lender, but they all have to come across the minimum guidelines set by Fannie and Freddie.

These standards give lenders and investors more conviction in these loans.

As a result, conforming loans are available with ultra–low mortgage rates and merely 3% down payment.

What if my loan is over the conventional limit?

Remember that the conforming loan limit applies to the loan amount, not the home cost.

For instance, say a buyer is purchasing a i–unit home in Boulder, Colorado where the limit is $747,500. The home cost is $1 million, and the buyer is putting $400,000 downwards.

This buyer is eligible for a befitting loan. The final loan amount is $600,000 – well within limits for the area.

Still, many applicants will demand financing above their local loan limit. For them, a number of solutions be.

Jumbo loans

The simplest method is to use a jumbo loan. Jumbo mortgages describe any home loan above local befitting limits.

Using the case in a higher place, permit'south say the Boulder, CO home buyer puts downwards $200,000 on a $1 million domicile. In this instance, their loan amount would be $800,000 – above the local befitting loan limit of $747,500. This heir-apparent would need to finance their home buy with a colossal loan.

You might think jumbo mortgages would accept higher interest rates, simply that's not e'er the instance.

Jumbo loan rates are often nearly or even below conventional mortgage rates.

The catch? It's harder to qualify for jumbo financing. You'll probable need a credit score above 700 and a down payment of at least ten–20%.

If you put down less than twenty% on a jumbo abode purchase, you'll also have to pay for private mortgage insurance (PMI). This would increment your monthly payments and overall loan toll.

The side by side method helps y'all avoid PMI when buying above conforming loan limits.

Piggyback financing for high–priced homes

Possibly the virtually price–effective method is to choose a piggyback loan. The piggyback or "80/10/10" loan is a blazon of financing in which a first and second mortgage are opened at the same fourth dimension.

Typically, this structure is used to avert private mortgage insurance.

A buyer can become an 80 percent first mortgage, 10 percent 2nd mortgage (typically a habitation disinterestedness line of credit), and put 10 percent down.

Nevertheless, these loans are also available for those putting twenty percent down or more. Here's how it would piece of work.

- Home price: $850,000

- Downwards payment: $170,000 (twenty%)

- Financing needed: $680,000

- Local conforming limit: $647,200

The buyer could construction their loan as follows.

- Downward payment: $170,000

- 1st mortgage: $647,200

- 2nd mortgage: $32,800

The habitation is purchased with a befitting loan and a smaller second mortgage. The commencement mortgage may come up with amend terms than a colossal loan, and the 2nd mortgage offers a great charge per unit, too.

What's the colossal loan limit for 2022?

Technically at that place's no jumbo loan limit for 2022.

Since jumbo mortgages are above the conforming loan limit, they're considered "non–conforming" and are non eligible for lenders to assign to Fannie Mae or Freddie Mac upon closing.

That means the lenders offering jumbo loans are gratis to gear up their ain criteria, including loan limits.

For example, one lender might set its jumbo loan limit at $two million, while some other might fix no limit at all and be willing to finance homes worth tens of millions.

Merely the amount you lot can infringe via a jumbo or non–conforming loan is limited by your finances.

You need enough income to make the monthly mortgage payments on your new home. And your debt–to–income ratio (including your futurity mortgage payment) tin can't exceed the lender'due south maximum.

You lot tin can use a mortgage estimator to gauge the maximum home toll yous tin likely afford. Or contact a mortgage lender to get a more accurate number.

What if I'grand getting an FHA loan?

FHA loans come with their own loan limits. Standard FHA limits for 2022 are listed below.

- one–unit homes: $420,680

- 2–unit homes: $538,650

- 3–unit homes: $651,050

- 4–unit homes: $809,150

You might notice that FHA'southward limits are considerably lower than the befitting limits. That'south by design.

The FHA program, backed by the Federal Housing Administration, is meant for home buyers with moderate incomes and credit scores.

But the FHA besides suits home buyers in expensive counties. Single–family FHA loan limits reach $970,800 in high–cost areas within the continental U.S. and a surprising $1,456,200 for a 1–unit of measurement home in Alaska, Hawaii, Guam, or the Virgin Islands.

What are today'southward conentional mortgage rates?

Mortgage rates for conventional conforming loans are stellar, which is why then many buyers consider a conforming loan before using jumbo financing.

Become a rate quote for your standard or extended–limit conforming loan. Compare to jumbo rates and piggyback mortgage rates to make sure you're getting the best value.

The information contained on The Mortgage Reports website is for informational purposes just and is non an advertising for products offered by Total Beaker. The views and opinions expressed herein are those of the author and practise non reflect the policy or position of Full Chalice, its officers, parent, or affiliates.

Source: https://themortgagereports.com/27773/2017-conforming-mortgage-loan-limits-fannie-mae-freddie-mac

Posted by: sutterdeupok.blogspot.com

0 Response to "Will Conforming Loan Limits Change In 2021"

Post a Comment